Economics Terms A-Z

Goods Market Equilibrium

Read a summary or generate practice questions using the INOMICS AI tool

The “goods market” is a vague-sounding (and rather poorly named) term in economics that is nevertheless an important macroeconomic concept. Goods market equilibrium refers to the idea that, in an economy, there is equilibrium between how many goods consumers want to buy and how many goods producers want to supply.

This means that supply and demand are balanced. There is no excess demand, no supply surplus, and no problems: everyone can participate in the market transactions they want to. This is only possible if aggregate demand and aggregate supply are equal (AD = AS; we assume in this article that short and long-run aggregate supply are the same).

This also happens to be the point where desired national savings and desired national investment are in equilibrium at a certain interest rate. Understanding how these concepts are intertwined is important for intermediate macroeconomics students, so let’s dive in.

National savings and the goods market equilibrium condition

The goods market equilibrium is often defined in economics textbooks as the point where “desired national savings” equals “desired national investment”, sometimes referencing the savings-investment identity, since the identity describes how investments must equal savings. Some authors or textbooks might introduce these concepts together. But this identity doesn’t seem to be at all related to product markets or the point where AD = AS, so let’s examine further.

Goods market equilibrium emerges from a description of GDP that uses the same equation as that for aggregate demand: Y = C + I + G + NX. In short, one of the methods for calculating GDP is to sum up spending in the economy, including consumption spending C, investment spending I, government spending G, and – you guessed it – net spending on trade NX. By this logic, GDP can be thought of as the sum of all spending in the economy, since all money is either spent to acquire goods or is “spent” on savings, which fuels investment spending.

The savings-investment identity in this construction of GDP describes that spending on investment is fueled by savings, and thus that savings really represents investment spending. Therefore calculating GDP by focusing on spending does not exclude savings.

Let’s start by examining the market equilibrium using algebra. The goods market is in equilibrium when AD = AS. This is also the point where the economy is producing at its full employment potential output Y.

The equation for Y is as follows: Y = C + I + G (we ignore trade and assume the economy is in autarky here, for simplification). For a full explanation on this equation, see the article on aggregate demand.

We adjust this equation to the following to prove that at the goods market equilibrium, desired national saving is equal to desired national investment and the savings-investment identity holds. It becomes: Yd = Cd + Id + G. Here, the d superscript indicates the desired level of the variable, such that Yd is desired output, etc. As a simplification, government spending G is assumed to be exogenous.

Now, just as with the savings-investment identity, subtract to yield: Yd - Cd - G = Id.

To finish our analysis, we must realize that the left-hand side of this equation is simply desired national savings. That’s because all income must be spent in one of three ways: buying goods and services, saving, or taxes. Notice that Yd represents total output, which is the same as total income for all agents in the economy. Now that we’ve subtracted two of the three ways income can be spent from it on the left-hand side, we’re left with only savings as the last portion of income that wasn’t spent on taxes or consumption.

Therefore, Sd = Yd - Cd - G = Id. This is the goods market equilibrium, and it shows that the savings-investment identity must hold. It also has an effect on interest rates in the economy. That’s because the amount of savings desired – which is another name for the demand for savings – has an effect on the interest rate. If more savings are desired, real interest rates will be pressured down, and vice versa.

The goods market and interest rates

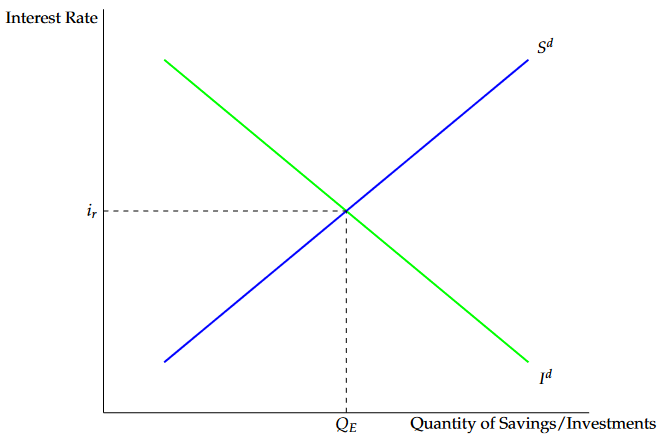

Seeing the goods market equilibrium depicted graphically is very useful to see how it affects interest rates. Again, this equilibrium describes a situation where AD = AS and desired savings is equal to national investment. See Figure 1 below for a depiction.

Figure 1: equilibrium in the goods market

In Figure 1, QE shows the equilibrium point where the real interest rate balances out the quantity of savings and investments desired. Sd represents desired savings at every real interest rate, while Id represents desired investment at each real interest rate. As the interest rate rises, the quantity of savings desired increases while the quantity of investment desired decreases.

Recall that the interest rate represents the cost of borrowing, and functions similarly to a “price” for taking on debt – in other words, the interest rate can be thought of as the cost of investing (naturally, this is a simplification and does not cover every usage or nuance of the relationship between the interest rate and the amount of economic investment. That’s fine for our learning purposes). It also represents the return to savings.

When the interest rate rises above the equilibrium level, the cost of borrowing is increased, and so the demand decreases for borrowing in the market for loanable funds. Meanwhile, the return on saved money increases, which leads to an increase in the amount of desired savings. In this case, the market is in disequilibrium because there is an excess supply of savings ready to be lent out, and a lack of demand for borrowing those savings to fuel investment.

Then, the interest rate will be pressured downward by market forces, as savers accept lower interest rates in order to actually secure a savings account, since banks facing excess demand for savings could lower interest rates and still find customers. Further, banks would be incentivized to lower the cost of borrowing to find borrowers and make loans, and would agree to lower interest rates to do so. These forces will pressure the interest rate down, until it eventually returns to equilibrium.

In summary

There are many moving pieces in this summary of the goods market. So, to recap: the goods market equilibrium describes the point where the demand for goods and services is equal to the supply of goods, in other words where AD = AS, which is influenced by the interest rate. This is also the point where desired national savings and desired national investment are equal, and where the loanable funds market is in equilibrium. Thus, in this state market forces have perfectly balanced the amount that economic agents want to buy, save, or invest.

If the interest rate is too high, individuals will be incentivized to save more and therefore purchase less (AD is pressured downwards and there is an excess supply of loanable funds), while firms will be incentivized to borrow and invest less, and vice versa. This changes the equilibrium until market forces bring the interest rate at a point where it is in equilibrium again.

Good to Know

Because the goods market equilibrium is defined where AD = AS, it will change when shocks to aggregate demand or aggregate supply change the equilibrium in those markets. This can include things like a change in consumer preferences, sudden changes in wealth, changes in the velocity of circulation, government policy changes, natural disasters, etc.

-

- PhD Candidate Job

- Posted 2 days ago

PhD Position in Macroeconomics

At Institute of Economics, University of Hohenheim in Stuttgart, Alemania

-

- Conferencia

- Posted 1 month ago

48th RSEP International Conference on Economics, Finance and Business

Between 1 Oct and 2 Oct in Rome, Italia

-

- Assistant Professor / Lecturer Job, Postdoc Job

- Posted 1 month ago

Assistant professorship(s) in the fields of accounting and finance at Department of Business Development and Technology

At Aarhus University in Herning, Dinamarca

Currently trending in Estados Unidos

Related Items

Próximas fechas de cierre

- Jul 31, 2026

- Jul 31, 2026

- Ago 01, 2026

- Ago 01, 2026

- Ago 05, 2026