Economics Terms A-Z

Price Elasticity of Supply

Read a summary or generate practice questions using the INOMICS AI tool

The price elasticity of supply for an item A ηA measures how the quantity of the item supplied qA changes in response to a change in the item’s price pA

\begin{equation*}

\eta_A = \frac{\Delta\mathit{q}_{A}}{\Delta\mathit{p}_{A}} = \frac{\frac{d{q}_{A}}{\mathit{q}_{A}}}{\frac{d{p}_{A}}{p}}

\end{equation*}

Price elasticity of supply is generally positive because firms are motivated to supply more (less) of an item as its price rises (falls). Precisely how sensitive supply is to changes in price depends on several factors. The most important is how long it takes sellers to adjust the amount of the item they can offer for sale. This is not just about the ability to ramp up production when more of the item is demanded. It is also about how feasible or costly it is for the seller to store items when demand falls.

The more complex the production process, the greater the dependence of sellers on other markets. Greater interdependence also increases the seller’s responsiveness to price changes. In markets for physical goods and the local provision of services, public infrastructure is also a significant factor in the price elasticity of supply.

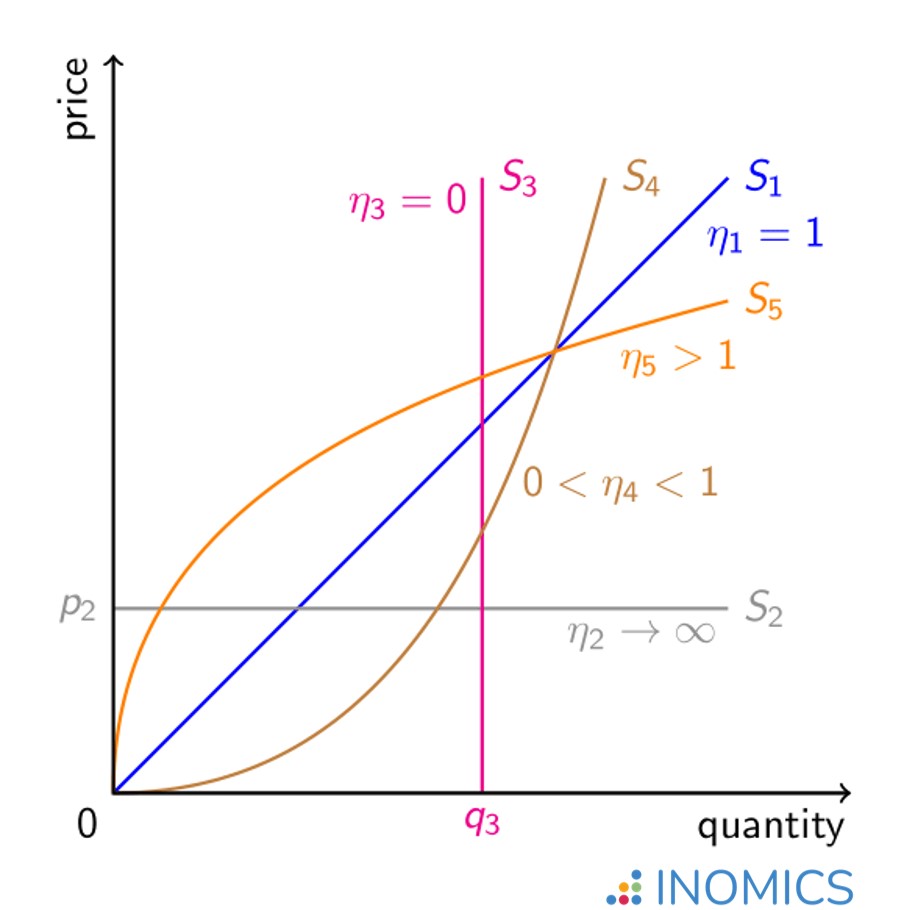

The supply curves for five standard theoretical cases are shown in the graph below. In the first case, the supply curve S1 starts at the origin (0,0), and is linear and upward-sloping. This implies that any change in price is met with a proportional change in quantity supplied. Therefore the price elasticity of supply is unitary η1 = 1. If the item’s price increases by 10%, so too does its quantity supplied.

As with the price elasticity of demand there are two extreme cases for the price elasticity of supply: perfect elasticity and perfect inelasticity. The horizontal supply curve S2 represents perfectly price-elastic supply: the elasticity tends towards (positive) infinity η2 → ∞.

In theory, this means that if its price increases above p2 then an infinite amount of the item will be supplied. But, if its price drops below p2 then none will be supplied. Clearly, this is unlikely to happen in practice. However, in industries with flexible production and factor markets with spare capacity, the price elasticity of supply can be very high.

One example is the market for coffee-to-go. In this market, new entrants are very quick to take advantage of increased consumer willingness to pay, and leave the market quickly when conditions deteriorate.

Figure 1: Various price elasticities of supply

At the other extreme, the vertical supply curve S3 indicates that supply of the item is fixed at a quantity of q3, whatever its price: supply is perfectly price-inelastic η3 = 0. This is the case, at least in the short-term, for items with longer, less flexible production processes. Indeed, producers of such items are unable to react quickly to price changes.

The remaining two cases are the supply curves S4 and S5. The former represents relatively price-inelastic supply 0 < η4 < 1. This can be seen by interpreting the graph: as the price increases, quantity increases only slightly. The latter shows a price elasticity of supply greater than unity η5 > 1. In contrast to S4, as the price increases, the quantity according to curve S5 increases by much more.

Economists distinguish between short-run and long-run supply curves due to the difference in their price elasticities. In the short run, supply is often assumed to be price-inelastic because the short run is defined by there being at least one fixed factor of production. In the long run, all inputs are variable and therefore supply tends to be more price-elastic, reflected in a flatter supply curve.

Further reading

The market for housing is a good example to gain an understanding of what can influence the price elasticity of supply. Using urban variation across the United States, Green, Malpezzi and Mayo uncover some key determinants of supply price elasticity in their article, “Metropolitan-specific estimates of the price elasticity of supply of housing, and their sources” (American Economic Review, 2005).

Good to know

The combination of price elasticity of demand and price elasticity of supply is what determines the respective sizes of consumer surplus and producer surplus in a market.

In general, the less price-elastic demand (supply) is, the greater the consumer (producer) surplus. This is particularly relevant information when it comes to market interventions because it allows one to calculate which side of the market stands to gain most (or, more commonly, lose least) through a tax or other regulation on supply.

-

- Postdoc Job

- Posted 4 weeks ago

Postdoc (m/f/x)

in Trier, Germany

-

- Research Assistant / Technician Job

- Posted 4 weeks ago

Research Assistant: Foreign and Defense Policy; Demographics and Political Economy

At American Enterprise Institute in Washington, United States

-

- Conference

- Posted 2 weeks ago

MIRDEC 27th Barcelona 2026 Conference

Between 24 Nov and 25 Nov in Barcelona, Spain

-

-

Currently trending in United States

Related Items

-

Call for applications - PhD Program at the University of Basel Graduate School of Business and Economics

-

Call for Expressions of Interest Tenure-Track Assistant Professor (RTT) in Economics, Management, and Statistics

-

Special Conference on Trade Wars, Geopolitical Fragmentation and Repercussions for Financial and Monetary Stability

Upcoming Deadlines

- Aug 05, 2026

- Aug 07, 2026

- Aug 07, 2026

- Aug 10, 2026

- Aug 14, 2026