Economics Terms A-Z

Oligopoly

Read a summary or generate practice questions using the INOMICS AI tool

An oligopoly is a market in which there are only a few sellers of the item being traded. The decisions of one seller thus affect the decisions of the other sellers in the market. Sellers compete strategically in the market by taking each other’s interests and actions into account.

Markets for goods and services have varying numbers of sellers, ranging from one (monopoly) to infinitely many (perfect competition). Oligopoly lies somewhere in between. In practice, industries with between two (duopoly) and six major players are considered to be in oligopolistic competition. Examples of oligopoly include the markets for mobile telephone networks such as Deutsche Telekom, Orange, Telefónica and Vodafone in Europe, the market for large passenger aircraft like Airbus and Boeing, and the market for soft drinks like Coca Cola and PepsiCo.

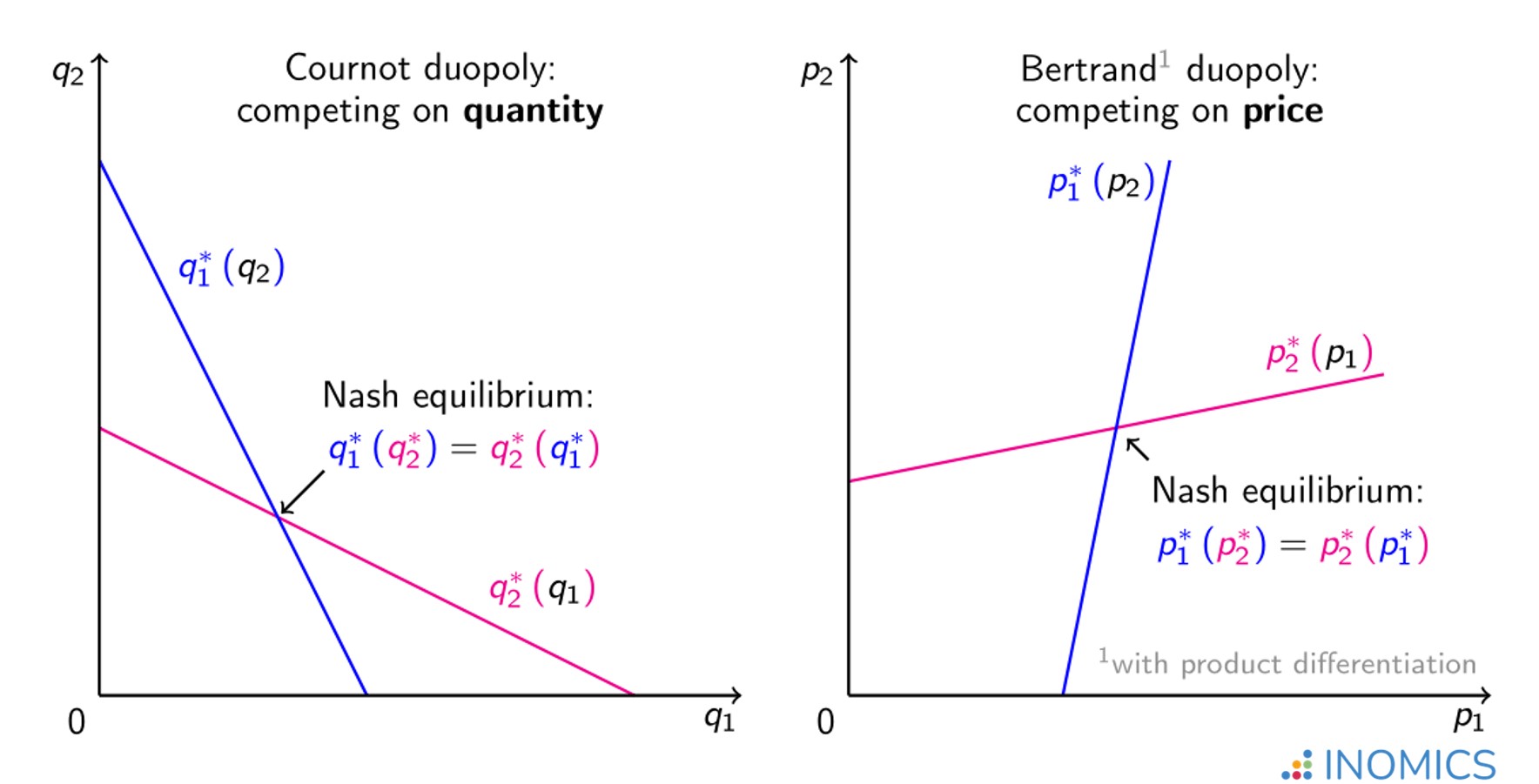

The theory of oligopoly originated in 1838. French polymath Antoine Augustin Cournot observed a market for mineral water, which had two firms competing for market share. Realizing that neither firm could ignore the other’s supply of water in the market, Cournot analyzed the market as a game in which the quantity supplied by one firm q1 is a direct function of the quantity supplied by the other q2, i.e. reaction function q1*(q2) as shown in the graph on the left.

Assuming that each firm sells an identical or homogenous product, faces identical costs and that the firms act simultaneously, equilibrium quantities supplied in the market are determined where the reaction functions cross q1*(q2*) = q2*(q1*). This was the first formal representation of a Nash equilibrium. It was over a century before John Nash published his general proof.

In Cournot equilibrium, both firms make a positive profit and the market is supplied with more of the item at a lower price than in monopoly, but less of the item and at a higher price than in a perfectly competitive market.

Figure 1: Nash equilibrium comparison between Cournot and Bertrand market scenarios

Forty-five years later in 1883, another French professor, Joseph Louis François Bertrand, contended that Cournot’s analysis of oligopolistic competition was unrealistic since firms more commonly compete not on quantity but on price in the real world.

Under the same assumptions of identical products or services, identical costs and simultaneous decision-making, Bertrand demonstrated how price competition in an oligopoly would instead result in zero profits for the firms, where prices would be set equal to marginal cost, just as in perfectly competitive markets. For this reason, firms in an oligopoly have an incentive to differentiate their products to a certain extent in order to profit from different buyers’ individual preferences. Some buyers will then not consider the products offered by each firm as perfect substitutes, rather they will be imperfect substitutes in consumption.

The graph on the right shows the reaction functions of two firms in a duopoly where they offer similar but not fully identical products and compete on price. Note how in this situation, if one firm increases (decreases) its price, this prompts the other firm to raise (lower) its price as well. This contrasts with the Cournot case, where if one firm increases its market share (quantity), the other responds by reducing its supply in the market.

As with Cournot, the Nash equilibrium in the Bertrand duopoly with product differentiation is at the point where the reaction functions cross and prices are set at p1*(p2*) = p2*(p1*).

In real oligopolies, firms compete both by varying price and by varying quantity supplied. It may be argued that firms with long production processes, as in the case of passenger-aircraft manufacturers Airbus and Boeing, make strategic decisions about quantities supplied in the market rather than their prices (which can be adjusted later) and thus come closer to Cournot competition.

On the other hand, market leaders that can vary their production at short notice, such as drinks manufacturers, are more likely to compete directly on price and hence fit the Bertrand competition model better. And in order to avoid suffering from zero profits, Coca Cola and PepsiCo do their utmost to convince us that their drinks are not identical!

Further reading

Jean Tirole won the Nobel Prize in Economics in 2014 for his for his analysis of market power and regulation. For a comprehensive treatment of oligopolistic competition, see chapter 5 of his text book, “The theory of industrial organization” (MIT Press, 1988).

Good to know

Rather than slaying each other in vicious price wars, firms competing in oligopolistic markets are often tempted to collaborate in pricing strategy and to coordinate supply in the market, in some cases merging their operations into a single entity. While this can sometimes benefit the industry and lead to better products, market concentration, the formation of cartels and price-fixing can be detrimental to the consumer. See the article on antitrust policies for further details.

-

- Professor Job

- Posted 2 weeks ago

Professor, Economics

At Tyler Junior College in Tyler, United States

-

- Assistant Professor / Lecturer Job

- Posted 1 week ago

Assistant Professor - Economics

At Salisbury University in Salisbury, United States

-

- Event, Conference, PhD Candidate Job

- Posted 1 day ago

Tor Vergata Ph.D. Conference in Economics

At University of Rome Tor Vergata in Rome, Italy

Currently trending in United States

Related Items

-

Master in International and Monetary Economics (MIME) - Joint Program by the Universities of Basel and Bern

-

LM(EC)2 – Two year Master's programme in Economics and Econometrics – Alma Mater Studiorum - Università di Bologna

-

PAE – Two-year Master's program in Policy Analysis and Evaluation – Alma Mater Sturdiorum - Università di Bologna

Featured Announcements

Upcoming Deadlines

- Jul 15, 2026

- Jul 21, 2026

- Jul 26, 2026

- Jul 26, 2026

- Jul 29, 2026